By Aboubakr Kaira Barry, CFA, CPA — Managing Director, Results Associates, Bethesda, Maryland

President Tinubu is stabilizing the macroeconomy. A global benchmarking framework shows why that is not enough.

The Public Expenditure and Financial Accountability framework — PEFA — is the gold standard for measuring how well governments manage public money. Established in 2001 by seven founding partners including the World Bank, IMF, and European Commission, it grades 31 performance indicators (PIs) on a six-point scale: A (excellent) = 4.00; B+ (very good) = 3.50; B (good) = 3.00; C+ (satisfactory) = 2.50; C (basic) = 2.00; D+ (below basic) = 1.50; D (inadequate) = 1.00. A score of D* means data was too scarce to assess — itself a governance failure.

In 2022, Rwanda’s PEFA assessment averaged 3.12 out of 4.00, ranking it first among 32 African countries. Nigeria’s most recent assessment, completed in 2019, averaged 1.67, placing it 27th. The comparison is conservative: Nigeria’s 2019 score almost certainly overstates its current position. The Central Bank’s ways-and-means lending expanded from ₦6 trillion to ₦22 trillion outside the formal budget, COVID-19 procurement fraud was confirmed by Nigeria’s own anti-corruption commission, and no major PFM legislation was enacted in the interim. The 2019 PEFA score is not a baseline. It is a ceiling.

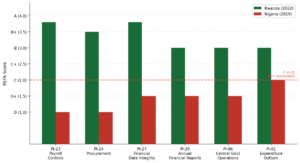

The scores reveal why. Rwanda scores at or near A on payroll controls (PI-23), procurement (PI-24), and financial data integrity (PI-27). Nigeria scores D across all payroll indicators — enabling ghost workers — D across all procurement indicators — enabling inflated contracts — and D on suspense account management, the classic transit route for misappropriation. Transparency International’s Corruption Perceptions Index mirrors this divergence: Rwanda ranks in the mid-40s globally; Nigeria ranked 150th in 2022. CPI captures the outcome; PEFA identifies the institutional doors left open.

Figure 1. Rwanda vs. Nigeria on six key PEFA indicators. Sources: PEFA national assessments (Rwanda 2022, Nigeria 2019). Red dashed line marks C (2.0), the minimum acceptable threshold.

President Tinubu’s reforms since May 2023 deserve genuine acknowledgement. Unifying the exchange rate, removing the fuel subsidy, and rebuilding gross reserves above $40 billion represent the most serious structural adjustment Nigeria has attempted in a generation. Federation revenues have nearly doubled year-on-year in some months. And yet the IMF projects real output per capita growth at around 0.6 percent in 2025. Debt service rivals the combined allocations for health, education, and infrastructure. More money flowing through D-rated systems does not produce better services. It produces larger leakages.

Three Structural Changes

Three structural changes are required, and none needs a constitutional amendment.

First, the President should establish a PFM Monitoring and Tracking Office within the Presidency, mandated to publish quarterly implementation scorecards for every federal PFM reform commitment. Its role is not to implement — that belongs to Finance, the Budget Office, and the OAGF. Its role is political accountability: making reform slippage visible at the apex.

Second, Nigeria should pass legislation establishing an independent Office of Budget Responsibility modelled on the UK’s OBR. An independent OBR scrutinizes budget assumptions and publishes findings without executive clearance — ensuring no government presents a budget built on implausible oil projections without an independent institution saying so publicly.

Third, while states have constitutional autonomy, the Federal Government possesses sufficient fiscal levers to promote expenditure accountability and resolve the perennial failure of states to release funds to local governments. Three instruments are available.

Fiscal Performance Weighting in the Revenue Sharing Formula

The Revenue Mobilisation Allocation and Fiscal Commission (RMAFC) reviews the Federation Account sharing formula periodically. Currently anchored on population, land mass, and equality of states, the formula should incorporate a fiscal performance score. States that publish audited accounts, demonstrate internally generated revenue growth, and comply with LGA remittance obligations would receive a marginally larger share; those that fail these benchmarks would receive marginally less.

PFM Conditionality on State Borrowing Approvals

The Debt Management Office approves state borrowing based principally on debt service capacity. The reform is straightforward: add fiscal governance conditions. Before a state receives DMO approval, it must demonstrate that its last two years of accounts have been audited and published, that it has not withheld LGA allocations, that it has adopted IPSAS (International Public Sector Accounting Standards), and that its debt-to-revenue ratio falls within a sustainable band.

Public Fiscal Performance Scorecard at NEC

The Federal Government should restructure National Economic Council meetings with state governors to incorporate a Public Fiscal Performance Scorecard — a league table covering each state across four dimensions: revenue generation performance; audit compliance status; expenditure quality and LGA allocation remittance; and debt sustainability position. The recommended Financial Management Office in the Presidency shall serve as secretariat, responsible for compiling, validating, and publishing the scorecard after each meeting — simultaneously to the press, civil society, and international partners including the World Bank and IMF.

The President should leverage the current legislative majority to pass the requisite laws. If the government could enact the recent tax reform bills, it can — with comparable political will — legislate the architecture of sound financial management, laying the foundation for Nigeria to become the leading nation it has the potential to be.

The distance between Nigeria’s 1.67 and Rwanda’s 3.12 is not merely a data point. It is the distance between revenues collected and services delivered. President Tinubu has done what his predecessors would not. But stabilizing the macroeconomy is the precondition for PFM reform, not a substitute for it. As Justice Louis Brandeis observed, sunlight is the greatest disinfectant. By bringing national visibility to these institutional failures and building the architecture for best-practice financial management, President Tinubu can lay the foundation for the effective utilization of Nigeria’s resources — and make the case that governance, not just growth, is what will make Nigeria great.

The author specializes in PEFA assessments and PFM reform in West Africa. Nigeria: 27th of 32 African countries assessed, score 1.67 (2019). Rwanda: 1st of 32, score 3.12 (2022).