By Aboubakr Kaira Barry, Managing Director, Results Associates, Bethesda, Maryland, USA

The exchange rate regime is usually a dry, technocratic choice. In West Africa today, however, it has become an existential fault line. The CFA franc’s convertibility to the euro (€1 = 655.957 CFA francs) still holds, but the foundations are increasingly strained. The real question is no longer whether the current configuration can last, but whether France and West African Monetary Union (WAEMU) countries choose a managed transition or wait for a shock to force change on worse terms.

This judgment rests on four structural factors that make the status quo progressively harder to sustain.

1. Fragile Reserve Foundations

The first factor is the fragility of the foreign exchange reserves that the Central Bank of the West African States (BCEAO) needs to defend the peg. Officials showcase a headline reserve of $24 billion following a rebound in late 2024, after a decline of $8.4 billion over the 2022–2023 period. This covers more than 60 percent of sight liabilities (currency in circulation plus bank reserves kept at the central bank)—three times the minimum requirement of 20 percent. However, import coverage stands at 4.2 months, hovering dangerously close to the IMF’s lower bound of 4.4 months.

Ultimately, what matters for a fixed exchange rate is not a single point in time, but the credibility of access to hard currency under stress.

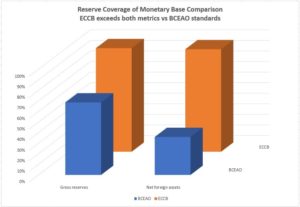

Recent IMF scenarios (Country Report 25/110, May 2025) show that under adverse financing or terms-of-trade shocks—such as oil export values dropping or gold and cocoa prices remaining at 2024 levels—WAEMU reserve coverage could fall below the minimum threshold, even after the current cyclical rebound. When net foreign assets are compared to the monetary base and benchmarked against the Eastern Caribbean Central Bank (ECCB), the region’s unencumbered reserves look much weaker than headline figures suggest.

[Chart 1: BCEAO and ECCB reserve contrast] – Source IMF

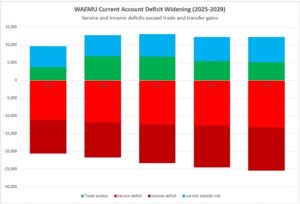

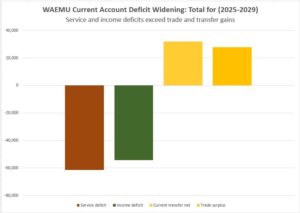

[Chart 2: Composition of current account balance] – Source IMF

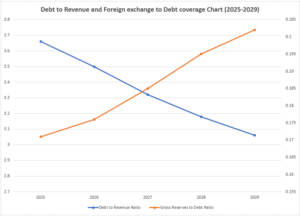

[Chart 3: Debt revenue and foreign exchange debt coverage ratio] – Source IMF

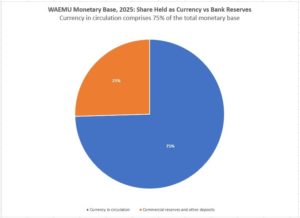

This will likely fail for three reasons. First, roughly 75 percent of the monetary base—money created by the central bank—circulates as currency with the public, limiting the BCEAO’s ability to monitor compliance effectively.

[WAEMU Monetary Base, 2025: Share Held as Currency vs Bank Reserves] – Source IMF

Finally, the reserve strategy depends on pooling: stronger members implicitly backstop weaker ones. As citizens in countries like Côte d’Ivoire and Senegal become more aware of intra-union imbalances, the political incentive grows to ring-fence national buffers rather than mutualize risk. The fracture line is no longer just France versus Africa; it could increasingly run between stronger and weaker members within WAEMU.

2. Weakening Political Support

The second structural factor is weakening political support on both sides of the Atlantic. In West Africa, a new generation of leaders in the Sahel and beyond has made sovereignty—and the costs and benefits of the CFA arrangement—central to their political narrative.

In France, the guarantee is provided in a currency Paris does not issue, under tight fiscal constraints. French government spending is reaching 57 percent of GDP, and populist sentiment is rising; the Rassemblement National (RN) is currently the largest single party group in the National Assembly. Meanwhile, WAEMU represents only a small share of French trade relative to its European partners.

History shows that exchange rate guarantees are only as strong as the political will behind them. From the collapse of the gold standard when President Nixon abruptly closed the gold window, to failed dollar pegs in Brazil, Thailand, Indonesia, Chile, and Argentina, governments have repeatedly abandoned fixed parities when reserves and domestic stability came into conflict. There is no evidence today that France intends to walk away from its commitments, but the political calculus is clearly more contested than it was two or three decades ago.

3. Existing Proposals Fall Short

Three solutions are on the table, and each faces serious limitations.

A simple return to pre-COVID fiscal rules (3 percent deficit ceilings, 70 percent debt-to-GDP), as recommended by the Council of Ministers in December 2024, ignores the reality that even the eurozone’s Stability and Growth Pact has been repeatedly bent by core members, and that WAEMU countries face far larger and more volatile external shocks.

Tightening monetary policy to protect reserves, as proposed by the IMF, runs into hard political limits once credit to governments, banks, and households comes under pressure. Recent BCEAO responses to crises have shown that under stress, monetary financing tends to re-emerge through various channels. In 2023, the BCEAO bought CFA 933 billion of bonds from banks, which were then used to purchase treasury bills and sovereign bonds.

A broader “Eco” currency incorporating Nigeria, as discussed in ECOWAS, would concentrate monetary power in a single, oil-dependent economy whose cycles are poorly correlated with the rest of the region—without a fiscal transfer union to share risk. This risks importing volatility rather than diversifying it.

4. WAEMU Is Not an Optimal Currency Area

Nobel laureate Robert Mundell argued that an optimal currency area should have symmetry of shocks, diversified economies, mobility of factors of production, and risk-sharing mechanisms. None of this exists in WAEMU. The economies are now bifurcating into oil and gas producers (Senegal, Côte d’Ivoire, Niger) and commodity producers (Burkina Faso, Mali), meaning there is no symmetry of shocks. They are neither diversified nor deeply integrated, with intra-regional trade amounting to less than 15 percent, compared with 60 percent in the eurozone.

If the status quo is increasingly costly and a Nigeria-dominated Eco is risky, the only credible strategic option left is a controlled return to national monetary sovereignty. This must be sequenced and supported so that small open economies do not simply swap an external anchor for domestic inflation. That credibility gap is precisely what a new transition facility must help bridge.

An SDR-Facilitated Transition

The debate is no longer just an economic calculation; it is a strategic political dilemma. All parties are trapped. There is, however, a viable off-ramp: a voluntary reallocation of Special Drawing Rights (SDRs) from WAEMU’s major trading partners to a special fund. This fund would provide long-term loans to countries that wish to leave the monetary union, enabling them to settle their obligations to the BCEAO and remaining members under clear, time-bound conditions.

This proposal is fiscally neutral for donors as it utilizes existing SDR holdings. Funding would come specifically from the 2021 COVID-19 general allocation, targeting the holdings of WAEMU’s major trading partners: Europe (France, Germany, and Italy) and China. Together, these nations received approximately 88.4 billion SDRs from that allocation (China 29.2 billion, Germany 25.5 billion, France 19.3 billion, Italy 14.4 billion), and hold cumulative SDR allocations of approximately 128 billion across all historical allocations.

The facility would be available to any WAEMU member choosing to exit. Access to the facility will be conditioned on the following:

- Banking Sector Consolidation

Strengthening the resilience of the financial system before exit, through:

- Consolidating weaker banks into stronger, better-capitalized institutions, in line with the BCEAO’s recent proposal to raise minimum capital to CFA 20 billion.

- Requiring credible resolution plans for systemically important banks, including clear loss-absorption hierarchies, so that failures can be managed without recourse to public bailouts.

2. No Bailout

There will be no bailouts in the first five years after exit.

- Fiscal Infrastructure and Transparency

A commitment to building a robust infrastructure for fiscal discipline and accounting transparency within seven years, comprising:

- Embedding a fiscal rule in the constitution limiting spending to long-term revenue to achieve a balanced or surplus budget over the medium term, with credible mechanisms for correction and narrowly defined escape clauses for extraordinary expenses.

- Implementing the Government Finance Statistics Manual 2014 (GFSM 2014) and accrual-based public accounts to ensure accurate, comprehensive data on fiscal outcomes.

- Reducing unexplained stock-flow adjustments, which currently amount to about 0.6 percent of GDP in the WAEMU region, through better recording of arrears, below-the-line operations, and valuation effects.

The facility will be operated as follows:

- IMF Management: The IMF would be designated manager of the facility. It would develop a framework for orderly exit from the monetary union and work with departing countries to build capacity for operating a central bank and an exchange rate regime suited to their circumstances (including institutional design, payment systems, and monetary policy operations).

- Loan Structure: The facility would provide long-term SDR-denominated loans for 20 years to pay for the net claim of the BCEAO—projected in 2025 to amount to CFA 12,760 billion (equivalent to SDR 17 billion)—and the reserves countries borrowed from the contributors. Upon exit, each country will receive: (i) the net foreign exchange reserves it contributed to the pool, and (ii) the SDR equivalent of net assets relating to the country. Thus, each central bank will start with reserves comprising these two types of liquid resources and a long-term SDR loan covering the amount borrowed to pay the BCEAO for the net domestic assets attributed to that country.

- Capping Debt: To prevent countries from accumulating additional obligations that the SDR facility would need to finance, borrowing from the BCEAO would be capped at each country’s current reserve position two years after the facility becomes operational. This ensures the facility finances existing obligations, not new debt accumulated during the transition process.

After exit, the IMF will incorporate the commitment to achieving fiscal discipline into its surveillance and link future financial assistance to meeting the agreed targets. Furthermore, to incentivize the realization of this important condition, countries that fully implement the infrastructure for fiscal discipline and transparency (the third condition for access) within 7 years will be rewarded with a reserve top-up equivalent to 1months of imports (SDR 4 billion for the 8 countries, based on the IMF’s calculations of reserve import coverage ratios).

For Europe and China: An Investment in Stability

For the international community, this is a low-cost insurance policy against geopolitical chaos.

For Europe, the Sahel is its demographic gateway. A disorderly monetary collapse would destroy middle-class savings and trigger migration on a scale dwarfing current flows. Reallocating SDRs—an asset that costs European treasuries almost nothing—is far cheaper than managing the aftermath of an economic implosion on Europe’s southern border.

For China, now WAEMU’s largest trading partner by bilateral trade volume, a currency crisis would paralyze supply chains and jeopardize repayment of infrastructure loans. Supporting an SDR facility aligns with Beijing’s desire to stabilize its overseas assets without direct military involvement.

The Path Forward

The success of this transition rests almost entirely on African agency. Technical solutions exist, but mobilizing the international political capital to unlock SDRs requires a new caliber of statesmanship from WAEMU leaders. They cannot wait for Paris, Beijing, or the IMF to offer a solution to a problem that threatens their own nations’ survival.

WAEMU heads of state must proactively engage key SDR-rich partners—Paris, Berlin, Rome, Beijing—with a unified proposition: limited, rules-based support now to engineer a controlled transition, or larger, messier interventions later when the system drifts into crisis. The inertia of the status quo is powerful, and the political risks of transition are real. But the alternative is to pretend that a regime designed for a different era can indefinitely absorb the combination of rising debt, shallow reserves, and political contestation.

It is up to West African leaders to seize this narrow window of relative calm. As George Washington once observed, “The challenge of leadership is to make the improbable inevitable.” The CFA franc system is not doomed to a chaotic end, but avoiding that outcome requires leaders who are willing to make the improbable choice of a sovereign, orderly exit—before events take that choice away.

Aboubakr Barry, CFA